|

1st Quarter 2003 |

When rates rise, how can income increase, but overall equity value fall?

|

||||

|

When rates rise, how can income increase, but overall equity value fall? |

History tells us that at some point in the future interest rates will begin to rise. How long it will be before that happens we don’t know. But, when it does occur, will it impact the level of earnings and the equity value of U.S. commercial banks? Fundamentally, interest rate risk (IRR) is the risk to earnings and capital arising from movements in interest rates. One fundamental way to quantify IRR is by stress-testing a one-year forecast of income and measure earnings at risk. This is generally considered a gauge of short-term IRR because it measures the effect changes in interest rates have on earnings over a one-year time horizon. But interest rate risk should be viewed from both a short-term and a long-term perspective. To measure long-term IRR we look at a similar measure called Equity Value-at-Risk. Equity Value-at-Risk is sometimes referred to as EVE at risk, which stands for "Economic Value of Equity at Risk". (See side bar) The impact of rising rates

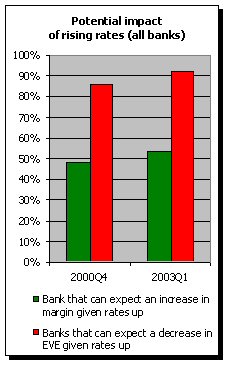

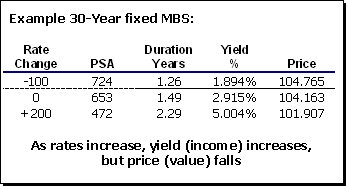

What is interesting about these statistics is that while nearly half of all banks are positioned to increase their margin given rising rates, over 75% of those banks will experience a drop in their EVE. To many bankers, examiners, auditors and analysts this situation seems contradictory. When rates rise does it make sense that short-term earnings will increase and long-term value will decrease? It does when you consider the effects of optionality. Protecting short-term losses The data in the table shows the prepayment speed, yield, duration, and price of a sample 30-Year Fixed MBS. As rates fall, prepayment speeds will increase. The faster prepayments will have two effects. First, they will shorten the duration of the security from 1.49 years to 1.26 years. Second, the yield will drop since there will be less principal available to earn interest. If rates begin to rise, prepayments are likely to slow down, which lengthens duration, and increases the yield. In a rising rate environment, the bank that owns this security will earn more than it would if rates remained level or fell.

Both short-term and long-term measures of IRR count Instruments with embedded options on the funding side also affect IRR. What will happen to earnings and EVE if CD early withdrawal rates rise sharply when market rates rise? How will the many flavors of FHLB advances (those with call dates, strike rates, etc.) impact a bank’s earnings and EVE when rates rise? With these types of “subtle” options increasingly finding their way onto banks’ balance sheets, it is more important than ever to monitor IRR from both a short-term and a long-term perspective. * Many investments that behave like this, i.e. many of those with options, are described as having negative convexity. |

|

|

This

A/L BENCHMARKS Industry Report article was published |

Unfortunately for many banks EVE will decrease given an increase in

market rates. In general, most community banks have longer duration assets

than liabilities. It is this inherent mismatch or difference in durations

that exposes the EVE of many banks to rising rates. From December 2000 to

March 2003 the percentage of banks with EVE at risk given rates up has

increased from 86% to 92%.

Unfortunately for many banks EVE will decrease given an increase in

market rates. In general, most community banks have longer duration assets

than liabilities. It is this inherent mismatch or difference in durations

that exposes the EVE of many banks to rising rates. From December 2000 to

March 2003 the percentage of banks with EVE at risk given rates up has

increased from 86% to 92%.  The trade-off is that as rates rise, the duration of this type of

security extends*. This lengthens the overall duration of the bank’s total

assets. A longer duration means that the value is more likely to decrease as

rates rise. As the bank’s asset value drops so does the EVE of the bank: E =

A – L.

The trade-off is that as rates rise, the duration of this type of

security extends*. This lengthens the overall duration of the bank’s total

assets. A longer duration means that the value is more likely to decrease as

rates rise. As the bank’s asset value drops so does the EVE of the bank: E =

A – L.